Signa Holding: the largest bankruptcy in Austrian history

- Mar 19

- 27 min read

I. Introduction

Few corporate collapses in recent European real estate have matched the scale, prestige, and symbolic weight of Signa Holding. Built by Austrian entrepreneur René Benko, the group grew into a vast property and retail empire with holdings that stretched from prime assets in the German speaking world to stakes in Selfridges and New York’s Chrysler Building. What had once looked like one of Europe’s most formidable private real estate platforms would, within a remarkably short period, become a case study in excess, opacity, and financial fragility.

When Signa Holding filed for insolvency in Vienna on 29 November 2023, debts of around 5 billion euros made the case the largest bankruptcy Austria had ever seen. The collapse did not remain confined to one holding company. It triggered a broader chain reaction across a dense network of real estate and retail entities, forcing creditors, courts, and administrators to disentangle a structure whose complexity had long been part of its aura. By September 2025, creditor claims against Signa Holding alone had reached 8.35 billion euros, although a large share remained disputed.

Yet the Signa story is not simply the story of a property group caught on the wrong side of a cycle. It is also the story of an empire built in an era of cheap money, rising valuations, abundant private capital, and exceptional social access. For years, Benko managed to attract prominent investors, lenders, and business families who saw Signa not merely as an investment platform, but as a privileged gateway into prime European real estate. That is precisely why its failure matters so much. The fall of Signa offers a rare and unsettling lens on leverage, governance, valuation, and the dangers of mistaking reputation for resilience.

II. The Beginning of the Story

René Benko did not emerge from the traditional ranks of European real estate dynasties. Born in Innsbruck in 1977, he came from an ordinary background, left school before graduation, and entered the property world at a young age by converting attics into apartments in Tyrol. In January 2000, he founded Immofina in Innsbruck, the company that would later become Signa. Even at this early stage, the essentials of the Benko method were already visible: a sharp instinct for underused assets, a preference for assets whose value could be transformed through repositioning, and an unusual ability to attract money and attention far beyond what his age and modest beginnings might have suggested.

What distinguished Benko from many small regional developers was not only his appetite for deals, but the way he sold a vision. Reuters relates that as early as 2003, he was using remarkably brazen language on his website to lure investors, promising that they could “earn money by doing nothing” and that it had “never been so boring to get rich.” Those slogans were clearly more than youthful provocation. They captured a style that would define Benko’s rise for two decades: confidence over caution, narrative over disclosure, and the presentation of property investing not as a patient craft, but as an almost frictionless machine for wealth creation.

The first years of the business were built on transactions that were small in scale compared with what would come later, but decisive in establishing both track record and ambition. Benko began with simple value enhancement, notably through attic conversions, and soon obtained a major financial boost from Austrian gas station heir Karl Kovarik. That injection of capital mattered because it pushed Benko beyond local opportunism and into a different category of operator.

The turning point in this first phase was Innsbruck itself. Benko’s acquisition and redevelopment of Kaufhaus Tyrol became the project that moved him from ambitious provincial investor to figure of national relevance. The building was redesigned by David Chipperfield and reopened after a major transformation, turning a dated department store into a modern retail landmark in the historic centre of Innsbruck. This mattered for more than symbolic reasons. Kaufhaus Tyrol showed that Benko could combine real estate, branding, architecture, and investor capital into a single story of urban renewal and value creation. It was also an early sign of one of Signa’s future strengths: the ability to attach prestige and narrative value to physical assets in prime locations.

From there, the scale increased quickly. By the end of the decade and the beginning of the next, Benko was moving into larger and more prestigious properties. Signa bought the corporate headquarters of Deutsche Börse in 2010, and in 2011 acquired KaDeWe in Berlin as part of a retail portfolio worth 1.1 billion euros. In Vienna, the group also accumulated landmark assets, including the historic BAWAG headquarters designed by Otto Wagner, while other central properties would become part of the broader “Golden Quarter” constellation that later symbolised Signa’s rise. What had begun as an Innsbruck story was rapidly becoming a cross-border empire with a strong focus on trophy locations and highly visible urban assets.

By this stage, the foundations of the future Signa galaxy were already in place. Benko had understood very early that scale in property does not come only from owning buildings. It also comes from mastering structure, perception, and access. As the company expanded from a small Tyrolean venture into a more elaborate holding platform, complexity itself became part of the model. More entities, more partners, more vehicles, and more strategic storytelling allowed Signa to present itself not simply as a property owner, but as a gateway to prime European real estate. The rise was built through a combination of transactional instinct, architectural symbolism and financial persuasion.

III. The Benko Galaxy at Its Peak

1. The architecture of the Signa empire

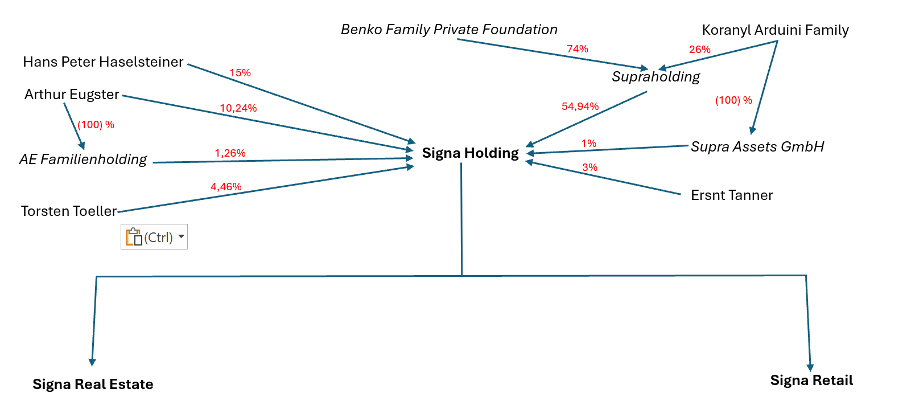

At its height, Signa was not simply a property company. It was a sprawling corporate constellation built around a central holding company and a series of specialised vehicles spanning trophy real estate, development, retail, and selected non-core holdings. In November 2023, just before the bankruptcy, the group had holdings worth 27 billion euros and a development pipeline of 25 billion euros, with real estate activities across Austria, Germany, Italy, Luxembourg, and Switzerland. The group was composed of roughly 1000 companies, which gives a sense of both its scale and its organisational density.

Organisational chart on the eve of Signa Holding's bankruptcy. Percentages based on aggregations from multiple sources (Austrian legal document, Orbis, Reuters, Bloomberg)

For individuals, it is possible that shareholdings are held through companies or holding companies with more than one owner (family groups, for example)

For AE Familienholding and Supra Assets GmbH, it is estimated that 100% is held by the family of Arthur Eugster on the one hand and the family of Koranyl Arduini on the other.

Within that structure, several pillars mattered most. Signa Prime Selection stood at the centre of the trophy property portfolio, while Signa Development Selection focused on new projects and large-scale urban developments. Alongside these stood the retail arms, notably Signa Premium and Signa Department Store, which brought major department store and luxury retail interests into the wider group. This architecture gave Signa a dual identity, with prime real estate on one side and department stores and shopping centres on the other.

The Chalet N and the Eden Reserve have been transferred to the Ingde Foundation in Liechtenstein in August 2023. The Foundation is registered in the name of the mother of René Benko.

2. Signa's external investors

Signa’s expansion was also inseparable from the network around René Benko himself. As can be seen with the external shareholders of the various companies in the Signa galaxy, René Benko managed to form a group of prominent backers and shareholders.

The Korányi-Arduini family is a very discreet and wealthy Brazilian Hungarian industrial dynasty residing in Switzerland, whose fortune originally came from the global cement industry before diversifying. The family was a minority shareholder in SupraHolding (26%) and directly in Signa Holding AG (1%) via Supra Assets GmbH.

Hans Peter Haselsteiner, one of Austria’s best-known industrialists and former chairman of Strabag (STR.VI), held 15% of Signa Holding.

Arthur Eugster, the CEO and co-founder of Eugster/Frismag AG had a total position of 11.5% in Signa Holding.

Torsten Toeller, the German entrepreneur and billionaire who founded Fressnapf (one of Europe's largest retail chains for pet supplies), held 4.46% of Signa Holding.

Ernst Tanner, CEO of Lindt & Sprüngli (LISN.SW) from 1993 to 2016 held another 3%.

The group's structure also made it possible to welcome minority investors into the various subsidiaries. This allowed the various Benko family foundations to retain control while benefiting from external equity capital at different levels of the group. Thus, in the Signa Real Estate division, we find, for example:

Klaus-Michael Kühne, German billionaire and logistics magnate who owns, among other things, 54.5% of Kühne + Nagel (KNIN.SW), 30% of Hapag-Lloyd (HLAG.DE), 15% of Lufthansa (LHA.DE) and 20.1% of Brenntag (BNR.DE). His real estate investments included a 10% stake in Signa Prime Selection AG.

Madison International Realty is a global real estate private equity firm headquartered in New York. It specialises in investments in high-end real estate. They also held a 5% stake in Signa Prime Selection AG.

The RAG-Stiftung is a German public-interest foundation tasked with financing the perpetual environmental liabilities of the country's former hard coal mining industry through its substantial investment portfolio of €17 billion. Prior to Signa's bankruptcy, the foundation held a 5% stake in Signa Prime Selection AG.

Peugeot Invest (PEUG.PA) is the Peugeot family's publicly traded investment company, which manages a diversified portfolio worth several billion euros, including a 7.7% stake in automotive giant Stellantis (STLA.MI). Beyond its traditional core business, the holding company has expanded its assets to include industrial and service leaders such as Groupe SEB (SK.PA), SPIE (SPIE.PA) and LISI (FII.PA), while maintaining key financial positions in Rothschild & Co and Tikehau Capital (TKO.PA). At the end of 2023, the holding company completely wrote down its 5% stake in Signa Prime Selection AG and 5% stake in Signa Development Selection AG, resulting in a loss of €300 million.

RFR Holding is a New York-based private real estate investment and development firm founded by Aby Rosen and Michael Fuchs that manages a world-class portfolio of over $10 billion, featuring iconic architectural landmarks such as the Seagram Building and the Chrysler Building, which they owned in a joint venture with Signa before the bankruptcy.

Central Group is a leading Thai multinational conglomerate owned by the Chirathivat family, operating as a global leader in the retail, real estate, and hospitality sectors. The group has consolidated its status as a leading luxury retailer by acquiring world-renowned department stores such as Selfridges in the United Kingdom, GLOBUS in Switzerland, and KaDeWe in Germany, taking full control over these assets following the bankruptcy of its former partner, Signa.

This shareholder constellation matters because it says something important about how Signa was perceived at its peak. Benko was not operating on the margins of European business. He had succeeded in bringing together a circle of investors whose names carried weight far beyond the real estate sector itself. Their presence gave Signa an aura of seriousness and embedded the group in a broader ecosystem of family wealth, industrial capital, and elite business networks across Austria, Germany, and Switzerland. Having such renowned investors on board certainly provided Signa and René Benko with a certain degree of ‘external validation’. The Financial Times revealed that German insurance companies had €3 billion exposure to Signa at the time of bankruptcy (in the form of shares and debt). It is reasonable to assume that many insurance managers were greatly reassured by the fact that Klaus Michael Kuhne, for example, had personally invested in Signa. The aura and reputation of Germany's richest man were seen as a guarantee of the seriousness of René Benko and his group, especially since he had said in 2022 that “Signa Prime is a blue chip among European real estate companies.”

3. Flagship assets and symbolic properties

The power of the Signa name rested largely on the prestige of the assets associated with it. These included Vienna's Goldenes Quartier, the Park Hyatt Vienna and the former Austrian Post Office building designed by Otto Wagner, Berlin's KaDeWe, Munich's Oberpollinger, Hamburg's Alsterhaus, Innsbruck's Kaufhaus Tyrol and, at group level, a stake in New York's Chrysler Building. It is precisely this concentration of recognisable and symbolic urban assets that has enabled Signa to project the image of a private European real estate champion rather than that of a conventional leveraged real estate operator.

The development side reinforced this image. The Elbtower in Hamburg and Vienna Twenty-Two, as well as other projects in Vienna, Berlin, Wolfsburg, Düsseldorf and Munich, were to be projects that would raise Signa's profile and consolidate its position as the best in European real estate. Even before the collapse, Signa's strategy was to control a pipeline of iconic developments in prime locations and use this pipeline to maintain the idea that the group was constantly expanding to the next level of elite urban real estate.

The Chrysler Building in New York

Chrysler Building New York / Photo: © Dominik Francis

4. Signa Sports United

A particularly revealing anecdote in the wider world of Signa is that of Signa Sports United (SSUNF), which illustrates how Benko's empire has expanded far beyond luxury real estate to embrace a much broader strategy. Signa Holding, through numerous subsidiaries, held just under 50 percent of the company. The company was formed as a group specialising in sports retail covering cycling, tennis, outdoor sports and team sports, bringing together brands and platforms such as Fahrrad.de, Bikester, Tennis Point, Campz, Addnature and, later, WiggleCRC. In June 2021, Signa Sports United agreed to go public in the United States through a merger with Yucaipa Acquisition Corporation, a special purpose acquisition company (SPAC), in a transaction that valued the group at approximately $3.2 billion and was expected to raise up to $645 million in gross proceeds. The transaction was completed on 14 December 2021, and the company began trading on the New York Stock Exchange the following day. At the time, the listing was presented as a means to fund growth, expand internationally and consolidate a fragmented sporting goods retail market through further acquisitions.

Yet Signa Sports United soon became one of the clearest examples of the gap between expansionary narrative and financial reality. By June 2023, the company reported €441 million in half year revenue but an adjusted EBITDA loss of €97 million, while also disclosing that it had secured a €150 million funding commitment from Signa Holding to support operations into fiscal year 2025. That dependence would prove fatal. On 2 October 2023, the company announced a strategic realignment, withdrew its medium-term guidance, and began the process of delisting from the NYSE. Just two weeks later, on 16 October, it disclosed that Signa Holding had terminated the very equity commitment on which management’s liquidity and going concern assumptions had rested, with €143 million still undrawn. Within days, major subsidiaries began filing for insolvency. In retrospect, Signa Sports United was more than a failed retail diversification. It was an early warning signal that parts of the wider Benko empire were already unable to survive without continuous internal support.

5. Why Signa became unavoidable

At its peak, Signa had achieved a status far greater than its mere size. It had become a platform that seemed to combine rarity, prestige and accessibility. Prime city-centre real estate assets, iconic luxury brands, ambitious development projects and a shareholder base comprising some of the best-known names in European business contributed to the impression that Signa occupied a privileged position in the market. In this sense, its appeal was not only financial. It was also social and symbolic. For many observers and participants, Signa seemed to offer a rare gateway to the high end of European real estate. The frenzied growth of the 2010s dispelled the doubts of even the most sceptical, who saw it as a perfect method for making money in an environment of zero or even negative interest rates.

Signa also offered something more than its competitors: direct, ultra-privileged access to the political world through its founder. Real estate is a complicated market, where building permits, purchase permits and work permits are often required. When you buy iconic department stores and build towers and buildings across the country, as in Austria or Germany, these relationships are essential and can determine the viability and feasibility of a project. This is how at least two former Austrian chancellors, Alfred Gusenbauer and Sebastian Kurz, worked directly with René Benko. The first sat on Signa Holding's group advisory board and the second is said to have facilitated certain operations for Benko and then to become one of his informal advisers/intermediaries. In Germany, we can mention Ole von Beust, former mayor of Hamburg, who has been advising Signa Prime since 2018, particularly about the Elbtower, a project strongly supported by Olaf Scholz, mayor of Hamburg at the time and future Chancellor of Germany.

Finally, the media, both traditional and business-oriented, have consistently portrayed René Benko in glowing terms throughout his career, describing him as the new real estate prodigy, repeating the incredible story of the 17-year-old boy who dropped out of school, worked hard renovating attics during the summer, and became a billionaire before the age of 40. For example, he was named Man of the Year by the Austrian business magazine Trend in 2012 and 2018, as well as Strategist of the Year by the German business magazine Handelsblatt in 2018. The renowned strategy consultant and founder of the company of the same name, Roland Berger, wrote the contribution.

IV. The Cracks Beneath the Surface

The first visible cracks in the Signa model appeared when the external environment changed. For years, European property had been supported by exceptionally low interest rates, abundant liquidity, and a market willing to finance large projects on generous terms. That regime ended abruptly. Reuters reported that the sharp rise in rates and construction costs brought the boom to a halt, drying up bank financing, freezing transactions, and pushing developers into distress across Europe. Signa, which had expanded aggressively during the era of ultra-low rates, was especially vulnerable once that environment reversed.

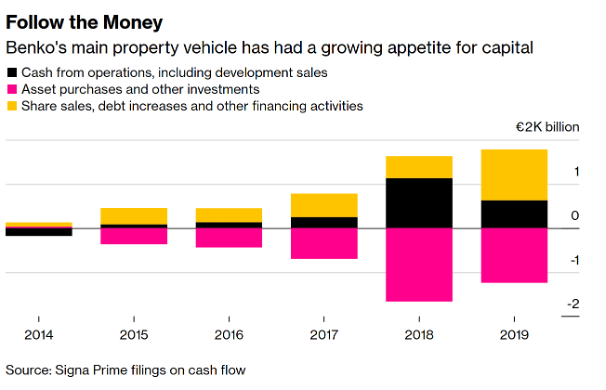

During the pandemic, the group was already exposed to weakening retail conditions, greater uncertainty around rental income, and a business model that remained closely tied to the continued appreciation of its prime assets. This point matters because it suggests that Signa’s apparent strength was never based solely on recurring operating performance. Even before the real estate market turned decisively, the group depended heavily on an environment in which valuations could keep moving upward and investors remained willing to fund the structure. Back in March 2021, journalist Boris Groendahl published a lengthy investigation into Signa in Bloomberg, in which he highlighted the limitations of the group's strategy and René Benko's headlong rush forward. The following graphs come from his article.

According to Bloomberg, the cumulative valuation gains at Signa Prime in 2021 had reached nearly 3.2 billion euros, while asset revaluations of 933 million euros helped drive a sharp rise in profit and supported a planned dividend of 201 million euros. But none of this means that the accounting treatment was improper. In real estate, fair value adjustments are normal. According to Boris Groendahl, Signa Prime's funds from operations (an approximation of recurring operating earnings in real estate, excluding valuation gains) had been negative every year since 2014. This means that all the Signa group's profits were due solely to an accounting revaluation of the value of its assets, which obviously does not generate cash. To finance growth, pay interest to creditors and dividends to shareholders, the only solutions were to borrow more money by pledging the real estate that had just increased in value or to raise even more funds from external investors. Here we can clearly see the rush forward that could only end badly.

This second chart strengthens that concern because it shows that these gains were not merely sitting on paper. Signa Prime distributed 634 million euros in dividends since 2014. As a result, investors who did not take the time to look closely at the accounts generally did not see the problem, seeing only the dividends increase each year. Signa's strategy therefore appeared to be highly successful when it combined an increase in the value of its assets with regular distributions to investors, but such a trend does not necessarily imply equally strong cash flow generation from operating activities. In retrospect, this is one of the most revealing characteristics of the Signa model.

Still in the same article, Bloomberg reported that valuations at Signa Prime were still expected to rise by about 10 percent in 2020 despite Covid. Even in a period of severe economic disruption, the group’s internal logic still relied on the continued upward repricing of prime assets. The vulnerability becomes easier to see. Signa’s strength depended not only on what it owned, but also on the assumption that the market would keep validating the values assigned to those assets. In November 2023 the construction had been suspended at six German development sites, including the Elbtower in Hamburg, after Signa fell behind on payments to its builder.

At the same time, falling valuations started to undermine the balance sheet logic on which so much of the group depended. Moody’s warned in December 2023 that Signa’s structure was “opaque and complicated” and that declining valuations of the pledged assets implied additional risks and potentially larger losses for lenders. According to Reuters, Signa Prime alone had debts of 4.5 billion euros against 54 properties valued at 19.3 billion euros, while later restructuring discussions centred on avoiding forced disposals of top assets. In a rising market, high valuations had supported leverage and expansion. In a falling market, that same mechanism worked in reverse.

The deeper problem, however, was that the economic substance of the group appears to have been weaker than the image projected by its asset base. This is partly an inference, but it is strongly supported by the liquidity picture that emerged once the market turned. In January 2024, Reuters reported that although Signa Prime could continue operating during insolvency proceedings, KSV1870, Austria’s leading creditor protection association, said that an additional 300 million to 500 million euros of liquidity would be needed in the short to medium term. Two months later, Austria’s government representative in the restructuring said that the company could remain afloat in the following weeks only by selling real estate.

This is where the distinction between accounting value and economic resilience becomes crucial. Signa had long presented itself as the owner and developer of prime assets whose value justified continual expansion. But property groups can report gains without generating corresponding cash, especially when valuation uplifts play a large role in reported performance. Therefore, according to Signa Holding’s administrator, the company had already been insolvent by November 2022 and estimated an operating loss of around 650 million euros in the year before the insolvency filing. In parallel, the Financial Times reported that creditors of Signa Development later alleged that the company had been weakened by large internal outflows and used as a financial reservoir for other parts of the group. Those allegations remain allegations, but they are consistent with a broader picture in which cash generation was far less robust than headline valuations suggested.

Seen in that light, the fall of Signa was not merely the consequence of bad timing. Rising rates, higher building costs, frozen financing markets, and stalled projects were the trigger. Yet the severity of the collapse points to something more fundamental: a business model that appears to have depended on buoyant valuations, fresh capital, and sustained market confidence to a far greater extent than many investors fully appreciated at the time. Once those conditions disappeared, the aura of permanence around the Benko empire began to dissolve with remarkable speed.

V. Bankruptcy, Asset Transfers, and Criminal Allegations

The formal collapse of Signa began at the top. On 29 November 2023, Signa Holding filed for insolvency in Vienna after last minute efforts to secure fresh funding failed. At the time, creditor protection associations put the holding company’s debts at around 5 billion euros. The proceedings initially affected 273 creditors and 42 employees, but it was already clear that the filing would not remain confined to one legal entity. Signa Holding sat at the centre of a web of hundreds of companies, and its insolvency immediately raised the prospect of a wider unravelling across the group’s real estate and retail operations.

That is exactly what followed. On 29 December 2023, Signa Development filed for insolvency in Vienna with debts of roughly 1.16 billion euros. The holding company belonged to a group of about 1000 companies, and that other divisions had already followed it into distress, making Signa the most important casualty of Europe’s real estate crisis. The complexity of ownership was not a side issue. It was one of the central problems of the insolvency itself. Creditors and administrators were forced to work through a structure in which liabilities, guarantees, holdings, and cash flows had long been spread across a dense corporate network. By late January 2024, claims against Signa Holding alone had already reached 8.61 billion euros, far above the roughly 5 billion euros initially flagged when insolvency was announced.

For a time, the main objective was to prevent a disorderly liquidation of the group’s crown jewels. In March 2024, creditors of Signa Prime and Signa Development backed restructuring plans intended to avoid a forced sale of top assets in Germany and Austria. The plan for Signa Prime gave a trustee up to five years to dispose of assets and aimed for recoveries of around 32 percent. Yet this did not amount to a rescue of the Signa model. It was an attempt to manage the wreckage more slowly and with less destruction than an immediate fire sale would have caused.

Even that managed unwinding proved fragile. At the end of December 2024, Austria’s Supreme Court rejected Signa Development’s restructuring plan, which meant the company had to enter bankruptcy proceedings. The broader holding level remained under administration as well. By September 2025, claims against Signa Holding stood at 8.35 billion euros, of which 2.8 billion had been recognised and 5.6 billion were disputed. Asset sales had raised only around 10 million euros, while further disposals, including stakes linked to the Chrysler Building and other holdings, were still under way.

Alongside the insolvency proceedings came allegations that pushed the case beyond the sphere of commercial failure and into criminal law. In January 2025, Austrian prosecutors arrested René Benko on suspicion of trying to hide assets from insolvency administrators and creditors. The prosecutors suspected him of secretly controlling a family trust and using it to conceal assets from the reach of the proceedings. Benko denied the allegations. That distinction is essential throughout the Signa affair. Insolvency is a fact. Criminal responsibility is a matter for courts, and many of the most serious accusations remain part of ongoing or recent proceedings rather than settled findings.

As the investigations widened, prosecutors identified several additional lines of inquiry. In June 2025, Austria’s anti-corruption and economic crime prosecutors said they had completed an initial investigation into the collapse and submitted their report so that decisions on possible prosecutions could be made. The four new strands included suspected favourable treatment of a creditor in connection with a repayment of roughly 15 million euros involving Signa Prime at a time when that unit was insolvent, suspected fraud related to the rental of a luxury chalet in Lech (the Chalet N), scrutiny of a 17 million euro loan to Signa Holding, and allegations of inflated prices in a Vienna residential project. Benko had previously denied the accusations. At the same time, insolvency administrators said they were preparing out of court negotiations to clarify liability issues and avoid long, expensive litigation where possible.

In October 2025, Benko went on trial in Innsbruck in the first criminal case linked to Signa’s collapse. The prosecutors described this as only a small part of a much wider investigation, with total suspected damage estimated at around 300 million euros. On 15 October 2025, an Austrian court convicted Benko of insolvency related fraud in that first case and sentenced him to two years in prison, finding that he had tried to keep 300 000 euros from creditors.

In December 2025, René Benko faced a second conviction, this time relating to luxury watches and cuff links hidden from creditors, which Benko also appealed. As of today, he remains in custody while wider proceedings and recovery efforts continued.

VI. What the Signa Case Reveals

The Signa case is significant because it was not simply a property crash. It was the failure of a belief system. At the heart of that system was René Benko, who successfully presented Signa as much more than a property group. Indeed, thanks to a combination of prestigious assets, ambitious projects, wealthy shareholders and close ties with major lenders, the group came to be seen as a privileged gateway to prime European real estate. In this sense, Signa was selling access and status as much as it was selling real estate.

This is where I think we can draw a comparison with Bernard Madoff and his Ponzi scheme. Bernard Madoff was also a self-taught financier with close ties to elite circles, whose reputation inspired extraordinary confidence in investors. People fought to invest their money in his fund, and he did everything he could to refuse their money, creating ever more frustration and reinforcing the desire to be a Madoff fund investor. What made this scandal so sensational was not only the promise of high returns, but also the belief that access to him was a guarantee of quality. Being in the Madoff fund was a source of great pride for many investors, a symbol of social success and belonging to a wealthy circle. René Benko, for his part, achieved something quite similar, at least in terms of attracting funds. For many of Benko’s shareholders, investing in Signa was a symbol of a certain social status and a guarantee of colossal returns with very little risk. While his system was not a Ponzi scheme in the strict sense of the term, he could not have been unaware that a system based solely on perpetual growth in asset value was not sustainable, and that distributing dividends when the company was not generating cash profits could not last forever.

This mechanism is particularly important because Signa's appeal to investors seems to have been partly self-reinforcing. The more prominent the shareholders, lenders, and business partners were, the easier it was for others to view their presence as a substitute for more thorough due diligence. Signa acquired such an aura that each new investor reinforced this illusion of security and legitimacy. What must be understood is that the vast majority of Signa's investors come from the same background. They are the economic elite of Germany, Switzerland, and Austria. These people socialize and talk to each other. When your entire circle of friends has invested in Signa and sees fabulous dividends coming in and explains how the value of the assets never goes down, you are naturally tempted to invest too. Similarly, when one German insurer lends to Signa, others are more likely to follow, considering that if the first one lent money, it must have done its due diligence. This was the situation Signa found itself in during all its years of growth, but it couldn't last forever.

This case also raises sensitive questions about gatekeepers. Moody's described Signa's structure as opaque and complicated in December 2023, just as the insolvency proceedings were expanding. Around the same time, Signa dissolved three key oversight bodies, including the group's executive committee, while the Financial Times reported that creditors of Signa's main entities wanted to remove management and hand control to independent auditors. In the Signa case, financial regulators, rating agencies, and auditors saw nothing (or chose to see nothing) before the bankruptcy. Was it René Benko's reputation that protected him from negative comments or warnings from his supervisory institutions, or did they once again fail to see anything coming, as in so many previous cases? We can hope that the various investigations will provide an answer.

In an effective system, one could argue that rating agencies should inform investors and reflect the various risks associated with the investment (particularly a downturn in the real estate market) in their ratings. For example, as mentioned above, Signa was bankrupt as early as November 2022, according to the liquidator of Signa Holding. How, then, can we explain that at the same time, Creditreform assigned Signa Prime Selection AG a rating of A-, while Fitch assigned Signa Development Selection AG a rating of B-/B+ and S&P a rating of B? Either the rating agencies misjudged Signa's accounts and the risks of bankruptcy, or the accounts were not representative of the situation, in which case why did the auditor KMPG approve them? It is certainly a combination of both, but it is legitimate to ask how this situation could have happened.

Another aspect of this case is René Benko's behaviour as the group sank into insolvency. The picture that emerges is that of a founder who, according to prosecutors and subsequent court proceedings, appears to have treated the line between personal wealth and debts with remarkable elasticity. Austrian authorities have claimed that Benko used family foundations and trust structures, such as the Laura Foundation (named after René Benko's eldest daughter), to shield his assets from receivers and creditors, with a total of €300 million transferred to entities linked to the foundation before the bankruptcy, according to the Financial Times. Another transaction under investigation was the sale of an Italian villa (Eden Reserves) to a Liechtenstein foundation linked to Benko's mother in exchange for shares in a Signa subsidiary that subsequently lost all their value. Benko has denied any wrongdoing and continues to appeal his convictions.

Prosecutors claimed that even as his financial situation deteriorated, Benko continued to spend on luxury items and attempted to protect his valuable assets from his creditors. For example, he allegedly paid a rent advance of €360 000 and donated €300 000 to relatives when his bankruptcy was imminent and investigators were examining hidden luxury goods, including furniture and a high-end watch. Prosecutors also accused him of hiding €120 000 in cash, as well as watches, cufflinks, and other valuables in a safe at a relative's home, which led to further charges of insolvency fraud. Such behaviour greatly damages the image of the passionate entrepreneur who made mistakes that Benko wants to convey.

VII. Conclusion

Signa's bankruptcy was not simply the collapse of a real estate group that had overextended itself. It was the implosion of a model based on ever-increasing valuations, abundant liquidity, the support of Europe's economic elite, and the belief that access to René Benko's world was a form of security. For years, this model seemed extremely successful. It brought together some of the most prestigious assets in European real estate, attracted wealthy families, insurers, bankers, and industrialists, and projected an image of permanence that few private groups in Europe could match.

Yet this apparent solidity hid a much more fragile reality. Signa's growth depended almost exclusively on valuation gains, fresh external capital, and a constant ability to maintain confidence. Once the market environment changed, the group's internal weaknesses became impossible to ignore. Rising interest rates, falling property values, slowing development, and tightening liquidity did not create the problem. They simply exposed a structure whose resilience had long been overestimated.

What makes the Signa case particularly striking is that it was not driven by naive or inexperienced investors. Many of the investors, lenders, and partners involved were among the most knowledgeable players in the German-speaking financial and business world. It is precisely for this reason that this case is so significant. Prestige, exclusivity, and social proximity can sometimes make critical scrutiny more difficult rather than easier. When enough respected names come into play, reputation itself can begin to substitute for proper analysis.

The final phase of the Signa case only reinforces this conclusion. The insolvency proceedings, the disputes over asset transfers, the role of family foundations, and the personal behaviour attributed to Benko all suggest that creditors were not simply dealing with a classic real estate bankruptcy. They were dealing with an opaque system that did not respect their rights.

In this sense, Signa deserves to be considered more than just the largest bankruptcy in Austrian history. It is a revealing case study on leverage, governance, valuation, and the social mechanisms of trust. It shows how powerful rhetoric, backed by elite networks and prestigious assets, can make it possible to avoid reality for many years.

Signa's bankruptcy should remind everyone of one simple thing. There is no such thing as a free lunch. The more irresistible an opportunity seems, the more necessary it becomes to ask fundamental questions rigorously and independently. Where does the money come from? Is the structure solid enough to withstand deteriorating conditions? Who really controls the assets? What is the valuation based on? These questions are rarely glamorous, but they remain, ultimately, the only reliable defence against the kind of illusion on which empires such as Signa are built.

VIII. Sources

Bilanz. (2023, March 5). Klaus Michael Kühne geht auf Distanz zu René Benko. https://www.bilanz.ch/bilanz/milliardar-uberdenkt-investment-klaus-michael-kuhne-geht-auf-distanz-zu-immobilienunternehmer-rene-benko-577691

Bloomberg News. (2020, October 6). Billionaire Benko due big payout after real estate revaluation. https://www.bloomberg.com/news/articles/2020-10-06/billionaire-benko-due-big-payout-after-real-estate-revaluation

Bloomberg News. (2021, March 31). Billionaire René Benko’s real estate empire at risk from COVID pandemic. https://www.bloomberg.com/news/features/2021-03-31/billionaire-rene-benko-s-real-estate-empire-at-risk-from-covid-pandemic

Die Presse. (2023, November 29). René Benkos Signa meldet Insolvenz an. https://www.diepresse.com/17868925/rene-benkos-signa-meldet-insolvenz-an

Financial Times. (2023, December 11). Insurers built €3bn exposure to struggling Signa property empire. https://www.ft.com/content/cae0ff11-01cb-48e2-badf-e4c192caf6b6

Financial Times. (2023, December 14). How Austria’s political elite helped René Benko’s rise. https://www.ft.com/content/e7fd7639-b364-4fba-bff7-6fbb82edf1ac

Financial Times. (2024, January 19). Signa group’s flagship German project falls into bankruptcy. https://www.ft.com/content/6e91f2b6-9b93-4cd3-bee9-b4613c5271af

Financial Times. (2024, January 25). Signa moved more than €300mn to René Benko linked entities before insolvency. https://www.ft.com/content/d36dce50-42a0-4197-a829-06f58d708a41

Financial Times. (2024, March 12). Signa company failed due to illicit financial transactions, creditors allege. https://www.ft.com/content/f887a1de-5171-4f61-9a89-cedc2f2d4c87

Financial Times. (2025, January 23). Property tycoon René Benko arrested in Austria. https://www.ft.com/content/361b3461-a621-4b99-9d4c-940d340d85ba

Financial Times. (2025, July 15). Bankrupt tycoon René Benko hit with criminal charges by Austrian prosecutor. https://www.ft.com/content/a2200443-e920-45d4-a14c-37b89b9d1594

Fitch Ratings. (2021, July 13). Fitch publishes Signa Development Selection AG’s “B-” IDR; rates unsecured bond “B+”/EXP. https://www.fitchratings.com/research/corporate-finance/fitch-publishes-signa-development-selection-ag-b-idr-rates-unsecured-bond-b-exp-13-07-2021

Kreditschutzverband von 1870. (2024, January 15). Insolvenz SIGNA Prime Selection AG. https://www.ksv.at/presse/laufende-insolvenzfaelle/insolvenz-signa-prime-selection-ag-sanierungsverfahren

NDR Doku. (n.d.). René Benko: Kaufhäuser und verschwundene Millionen [Video]. YouTube. https://www.youtube.com/watch?v=0p4fHB-gZRc

OTS. (2024, July 10). Signa Holding: Sonderverwalter hat Abschlussprüfer BDO geklagt. https://www.ots.at/presseaussendung/OTS_20240710_OTS0119/signa-holding-sonderverwalter-hat-abschlusspruefer-bdo-geklagt

Private Banking Magazin. (2024, January 3). 46 Versicherer laut Bafin bei Benko Unternehmen „exponiert”. https://www.private-banking-magazin.de/signa-insolvenzen-bafin-46-versicherer-exponiert-rene-benko/

Reuters. (2021, June 11). Signa Sports agrees SPAC deal, to buy Wiggle bicycle store: Source. https://www.reuters.com/business/retail-consumer/signa-sports-agrees-spac-deal-buy-wiggle-bicycle-store-source-2021-06-11/

Reuters. (2023, November 8). Explainer: How tycoon and Chrysler Building owner Benko lost grip of his empire. https://www.reuters.com/markets/europe/how-tycoon-chrysler-building-owner-benko-lost-grip-his-empire-2023-11-08/

Reuters. (2023, November 10). Benko’s Signa has halted work at six German projects, data shows. https://www.reuters.com/markets/europe/benkos-signa-has-halted-work-six-german-projects-data-shows-2023-11-10/

Reuters. (2023, November 29). Europe’s Signa toppled in property rout. https://www.reuters.com/markets/europe/austrias-signa-launch-self-administrated-insolvency-proceedings-2023-11-29/

Reuters. (2023, December 1). Benko’s complex web: Signa, Chrysler Building, Berlin landmark. https://www.reuters.com/markets/europe/benkos-complex-web-signa-chrysler-building-berlin-landmark-2023-12-01/

Reuters. (2023, December 6). Three more Signa companies file for insolvency as Moody’s warns on banks. https://www.reuters.com/markets/europe/signa-insolvency-is-credit-negative-some-banks-moodys-says-2023-12-06/

Reuters. (2023, December 18). Signa’s debts: A speaker’s fee, tax advice, and lawyers. https://www.reuters.com/business/signas-debts-speakers-fee-tax-advice-lawyers-2023-12-18/

Reuters. (2023, December 21). Property giant Signa dissolves three top oversight bodies. https://www.reuters.com/markets/europe/troubled-european-property-giant-signa-dissolves-two-top-oversight-bodies-2023-12-21/

Reuters. (2023, December 29). Signa Development files for insolvency with $1.3 bln in debts, KSV. https://www.reuters.com/markets/deals/signa-development-files-insolvency-with-13-bln-debts-ksv-2023-12-29/

Reuters. (2024, January 13). Property group Signa’s retail foray was a mistake, senior executive says. https://www.reuters.com/business/retail-consumer/property-group-signas-retail-foray-was-mistake-senior-executive-says-2024-01-13/

Reuters. (2024, January 15). Property group Signa’s Prime unit can fund operations, administrator says. https://www.reuters.com/world/europe/property-group-signas-prime-unit-can-fund-operations-administrator-says-2024-01-15/

Reuters. (2024, January 29). Signa Holding faces claims of $9 bln, insolvency manager. https://www.reuters.com/business/finance/signa-holding-faces-claims-9-bln-insolvency-manager-2024-01-29/

Reuters. (2024, March 13). Creditors could recover 32% of debt in Signa Prime restructuring plan. https://www.reuters.com/business/creditors-could-recover-32-debt-signa-prime-restructuring-plan-2024-03-13/

Reuters. (2024, March 18). Austria to reject Signa restructuring plan at creditor vote, says representative. https://www.reuters.com/markets/europe/austria-reject-signa-restructuring-plan-creditor-vote-says-representative-2024-03-18/

Reuters. (2024, December 30). Austria’s Signa Development heads for bankruptcy proceedings. https://www.reuters.com/markets/deals/austrias-signa-development-heads-bankruptcy-proceedings-2024-12-30/

Reuters. (2025, January 23). Austrian property tycoon Benko arrested, newspaper reports. https://www.reuters.com/world/europe/austrian-property-tycoon-benko-arrested-newspaper-reports-2025-01-23/

Reuters. (2025, January 23). Billionaire to bust: Austrian property tycoon Benko suffers new low with arrest. https://www.reuters.com/business/billionaire-bust-austrian-property-tycoon-benko-suffers-new-low-with-arrest-2025-01-23/

Reuters. (2025, January 24). Property tycoon Benko can remain in custody, Austrian court rules. https://www.reuters.com/world/europe/property-tycoon-benko-can-remain-custody-austrian-court-rules-2025-01-24/

Reuters. (2025, September 26). Benko’s insolvent Signa Holding faces creditor claims of 8.4 billion euros. https://www.reuters.com/business/finance/benkos-insolvent-signa-holding-faces-creditor-claims-84-billion-euros-2025-09-26/

Reuters. (2025, October 15). Austrian court gives ex-billionaire Benko two years’ prison for insolvency fraud. https://www.reuters.com/world/ruling-nears-austrian-fraud-trial-property-tycoon-benko-2025-10-15/

SIGNA Sports United N.V. (2021, December 14). Report of foreign private issuer pursuant to Rule 13a-16 or 15d-16 under the Securities Exchange Act of 1934 (Form 6-K). U.S. Securities and Exchange Commission. https://www.sec.gov/Archives/edgar/data/1869858/000119312521356909/d255920d6k.htm

SIGNA Sports United N.V. (2023, June 28). SIGNA Sports United N.V. reports H1 FY23 results. Business Wire. https://www.businesswire.com/news/home/20230628424068/en/SIGNA-Sports-United-N.V.-Reports-H1-FY23-Results

SIGNA Sports United N.V. (2023, October 16). SIGNA Sports United N.V. announces the termination of unconditional equity commitment letter by SIGNA Holding GmbH. Business Wire. https://www.businesswire.com/news/home/20231016051686/en/SIGNA-Sports-United-N.V.-Announces-the-Termination-of-Unconditional-Equity-Commitment-Letter-by-SIGNA-Holding-GmbH

SIGNA Sports United N.V. (2023, October 20). Tennis Point GmbH, one of the major subsidiaries of SIGNA Sports United N.V., files for insolvency, with further insolvency filings for other legal entities of the SIGNA Sports United Group, including SIGNA Sports United N.V., to follow. Business Wire. https://www.businesswire.com/news/home/20231019337651/en/Tennis-Point-GmbH-one-of-the-major-subsidiaries-of-SIGNA-Sports-United-N.V.-files-for-insolvency-with-further-insolvency-filings-for-other-legal-entities-of-the-SIGNA-Sports-United-Group-including-SIGNA-Sports-United-N.V.-to-follow

S&P Global Ratings. (2023, June 30). Research update: Signa Development Selection AG downgraded to “B-” from “B”; outlook negative. https://www.spglobal.com/ratings/en/regulatory/article/-/view/sourceId/12779192

WDR Doku. (n.d.). René Benkos Aufstieg zum Immobilienmogul [Video]. YouTube. https://www.youtube.com/watch?v=vbPar8MpC-k

ZDF MAGAZIN ROYALE. (n.d.). René Benko: Macht, Korruption, Milliardenpleite [Video]. YouTube. https://www.youtube.com/watch?v=SahyNbxEKPA

ZDFinfo Doku. (n.d.). Spiel mit Milliarden: Aufstieg und Fall eines Immobilien-Moguls [Video]. YouTube. https://www.youtube.com/watch?v=iDPKJYkjDrw

-

Written by Hippolyte Metzger-Otthoffer

Comments